All Categories

Featured

Table of Contents

On the various other hand, if a client requires to offer an unique requirements kid who might not have the ability to manage their very own cash, a trust fund can be included as a beneficiary, permitting the trustee to handle the distributions. The sort of beneficiary an annuity proprietor picks influences what the beneficiary can do with their inherited annuity and exactly how the proceeds will be exhausted.

Several contracts permit a spouse to determine what to do with the annuity after the proprietor passes away. A spouse can alter the annuity agreement right into their name, thinking all policies and rights to the preliminary arrangement and postponing immediate tax repercussions (Tax-deferred annuities). They can accumulate all continuing to be payments and any death benefits and choose recipients

When a spouse becomes the annuitant, the partner takes over the stream of settlements. Joint and survivor annuities additionally permit a called recipient to take over the contract in a stream of repayments, rather than a swelling sum.

A non-spouse can just access the designated funds from the annuity owner's first agreement. In estate planning, a "non-designated beneficiary" describes a non-person entity that can still be called a beneficiary. These include trusts, charities and various other organizations. Annuity proprietors can select to assign a trust fund as their recipient.

What is an Annuity Withdrawal Options?

These differences assign which beneficiary will obtain the whole survivor benefit. If the annuity proprietor or annuitant passes away and the key recipient is still active, the main recipient receives the fatality advantage. However, if the key beneficiary predeceases the annuity owner or annuitant, the survivor benefit will go to the contingent annuitant when the proprietor or annuitant passes away.

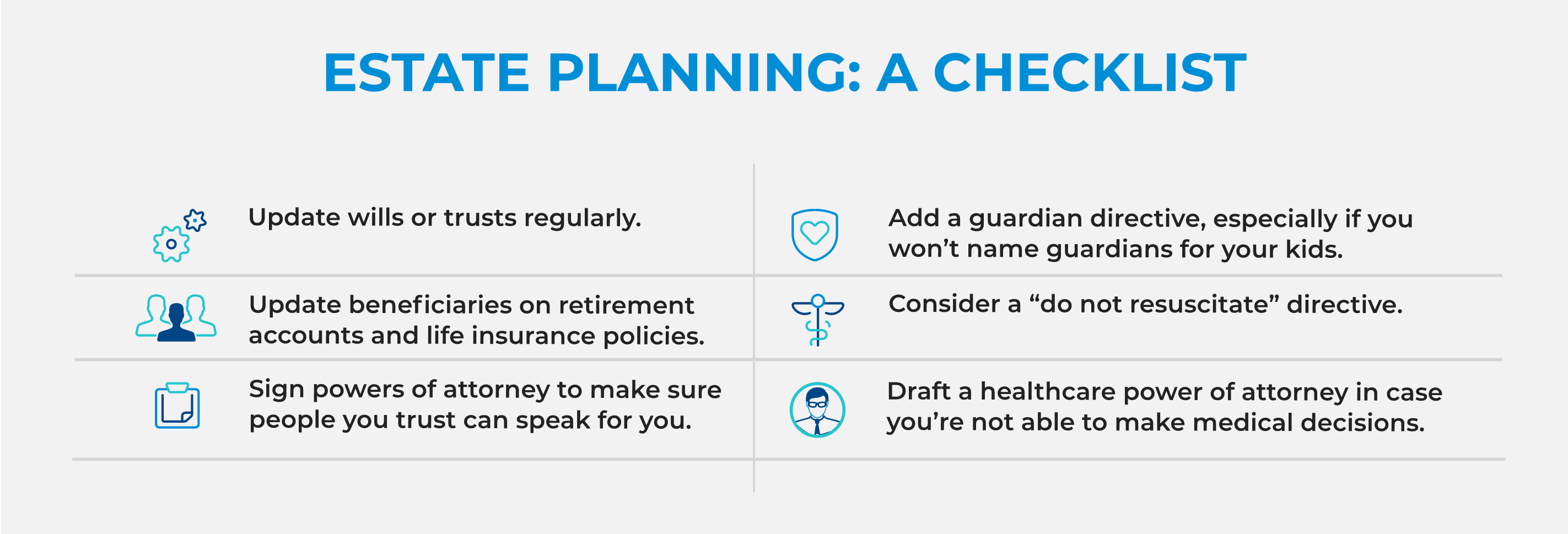

The owner can alter beneficiaries at any moment, as long as the contract does not need an irrevocable beneficiary to be named. According to professional factor, Aamir M. Chalisa, "it is necessary to comprehend the relevance of designating a beneficiary, as selecting the wrong beneficiary can have significant effects. Most of our customers choose to name their minor youngsters as beneficiaries, typically as the primary recipients in the absence of a spouse.

Proprietors who are married need to not presume their annuity immediately passes to their spouse. When choosing a recipient, take into consideration aspects such as your partnership with the person, their age and just how acquiring your annuity could affect their monetary situation.

The beneficiary's connection to the annuitant generally determines the rules they follow. A spousal recipient has even more options for dealing with an inherited annuity and is treated more leniently with taxation than a non-spouse recipient, such as a youngster or other family members member. Expect the owner does choose to call a kid or grandchild as a recipient to their annuity

What are the top Lifetime Payout Annuities providers in my area?

In estate preparation, a per stirpes designation specifies that, needs to your recipient die prior to you do, the beneficiary's offspring (youngsters, grandchildren, and so on) will get the survivor benefit. Connect with an annuity specialist. After you've picked and called your beneficiary or recipients, you must proceed to examine your selections at least yearly.

Maintaining your classifications up to day can make certain that your annuity will certainly be handled according to your wishes need to you pass away unexpectedly. A yearly evaluation, significant life events can trigger annuity owners to take an additional appearance at their recipient selections.

How can an Annuity Withdrawal Options protect my retirement?

Similar to any monetary product, looking for the assistance of an economic consultant can be beneficial. An economic planner can lead you via annuity management procedures, consisting of the techniques for updating your agreement's beneficiary. If no beneficiary is called, the payment of an annuity's fatality advantage goes to the estate of the annuity owner.

To make Wealthtender free for readers, we gain cash from advertisers, consisting of economic specialists and companies that pay to be included. This creates a dispute of passion when we prefer their promotion over others. Wealthtender is not a client of these economic services carriers.

As an author, it is just one of the most effective compliments you can provide me. And though I truly appreciate any one of you investing a few of your active days reviewing what I write, slapping for my post, and/or leaving appreciation in a comment, asking me to cover a subject for you really makes my day.

It's you claiming you trust me to cover a subject that's vital for you, which you're certain I 'd do so better than what you can already find on the Internet. Pretty heady things, and a duty I don't take likely. If I'm not aware of the subject, I investigate it on the internet and/or with contacts that know even more about it than I do.

Who has the best customer service for Income Protection Annuities?

In my friend's instance, she was thinking it would certainly be an insurance coverage of kinds if she ever goes right into nursing home care. Can you cover annuities in a post?" So, are annuities a valid recommendation, a shrewd move to protect guaranteed income permanently? Or are they an underhanded consultant's method of wooling unwary clients by convincing them to relocate assets from their portfolio right into a difficult insurance policy item pestered by extreme costs? In the most basic terms, an annuity is an insurance coverage item (that only certified agents may market) that ensures you month-to-month repayments.

How high is the surrender charge, and for how long does it use? This typically relates to variable annuities. The more cyclists you add, and the less risk you want to take, the reduced the repayments you ought to anticipate to receive for a provided costs. The insurer isn't doing this to take a loss (however, a little bit like an online casino, they're willing to shed on some customers, as long as they more than make up for it in higher profits on others).

What should I look for in an Variable Annuities plan?

Annuities chose correctly are the right choice for some people in some scenarios., and after that number out if any annuity alternative provides enough benefits to justify the costs. I used the calculator on 5/26/2022 to see what an immediate annuity could payment for a solitary costs of $100,000 when the insured and partner are both 60 and live in Maryland.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies Everything You Need to Know About Fixed Income Annuity Vs Variable Growth Annuity What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan W

Highlighting Fixed Income Annuity Vs Variable Growth Annuity A Comprehensive Guide to Retirement Income Fixed Vs Variable Annuity Breaking Down the Basics of Investment Plans Features of Smart Investm

Understanding What Is A Variable Annuity Vs A Fixed Annuity A Closer Look at How Retirement Planning Works Defining the Right Financial Strategy Advantages and Disadvantages of Variable Annuities Vs F

More

Latest Posts